Strait of Hormuz Crisis: What It Actually Means for Your E-Commerce Business

On February 28, 2026, the United States and Israel launched joint military strikes on Iran. Iran's Islamic Significant Guard Corps responded by closing the Strait of Hormuz to shipping. Three weeks later, the strait remains effectively shut, and the consequences are spreading through every layer of the global supply chain.

This is not a distant geopolitical event. If you sell physical products online, it is already affecting your costs, your delivery timelines, and your margins. Here is what the data actually shows.

What Happened and Why It Matters for E-Commerce

The Strait of Hormuz is a 21-mile-wide channel between Iran and Oman. It is the only sea route connecting the Persian Gulf to the open ocean. There is no bypass. Unlike the Suez Canal (which ships can route around via the Cape of Good Hope), Hormuz is a dead end. If it closes, everything inside the Gulf stays there.

Before the crisis, roughly 138 vessels transited the strait every day. As of March 6, that number dropped to single digits. By March 18, only 21 tankers had passed through since the war began. Iran has started allowing selective passage to allied nations, a handful of Indian, Saudi, and Chinese-flagged vessels, but the strait remains functionally closed to Western-allied shipping.

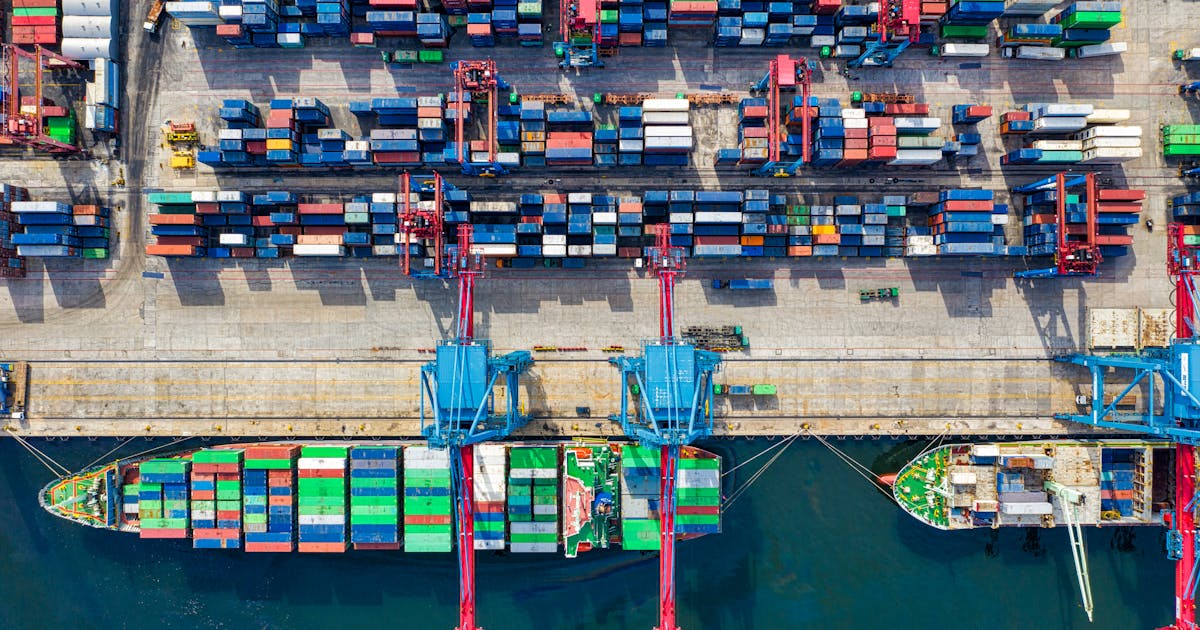

The Scale of What Is Trapped

The numbers are concrete:

- 450,000 TEU of container cargo trapped inside the Persian Gulf (1.4% of the global container fleet)

- 170 containerships unable to exit

- 150+ oil tankers anchored in open Gulf waters

- 14 LNG carriers slowed or stopped near the strait

- $4 billion in cargo value at immediate risk, with $877 million of that destined for US and European markets

- 40,000 seafarers stranded on vessels on either side

To put this in perspective: the 2021 Suez Canal blockage froze roughly $10 billion per day in trade for six days. The Hormuz closure has persisted for three weeks and removed 20% of global oil supply from the market, a disruption 3 to 5 times larger than the 1973 oil embargo by percentage of supply affected.

Oil Prices: The Engine Behind Every Cost Increase

Everything in e-commerce runs on oil. Shipping fuel. Warehouse electricity. Plastic packaging. Last-mile delivery trucks. When oil prices spike, every cost in your supply chain follows. For a deeper look at how fuel volatility cascades through operations, see our analysis of war, fuel prices, and e-commerce operations in 2026.

Where Oil Prices Stand

| Metric | Value |

|---|---|

| Pre-conflict Brent crude | ~$72/barrel |

| Peak price (March 2026) | $126/barrel |

| Current floor | Has not dropped below $100 since March 13 |

| Geopolitical risk premium | ~$40/barrel above fundamentals |

| US gasoline (national average) | $3.72/gallon (up from $2.90-$3.00) |

| Natural gas futures | Surged 40-74% |

Goldman Sachs projects $130/barrel in Q2 if the closure persists. Some analysts are no longer ruling out $200/barrel. The IEA and member states released 400 million barrels from emergency reserves on March 11, but that covers roughly 20 days of typical Hormuz flows. It buys time. It does not fix the problem. For ongoing freight rate analysis, Flexport's research portal tracks how energy prices flow into shipping costs.

Shipping Costs: The Numbers E-Commerce Sellers Need

Shipping cost increases hit e-commerce in three places: carrier surcharges, insurance premiums, and fuel surcharges. All three have spiked simultaneously.

Container Carrier Surcharges

| Carrier | Surcharge Type | 20ft Container | 40ft Container |

|---|---|---|---|

| Maersk | Emergency Freight Increase | $1,800 | $3,000 |

| CMA CGM | Emergency Conflict Surcharge | $2,000 | $3,000 |

| Hapag-Lloyd | War Risk Surcharge | $1,500/TEU | N/A |

| CMA CGM | Emergency Fuel Surcharge | $150-$265/TEU | N/A |

These stack. A single 40ft container from Asia that cost $2,200 in January can now carry $4,000-$7,000 in surcharges alone, before the base freight rate increase. The Freightos Baltic Index tracks these container rate movements in near real-time.

"Shipping costs from Hormuz disruptions: 20ft container Shanghai to LA jumped from $3k to $7.5k. Carrier quotes include $500 fuel spike premium. Blame oil volatility from ME conflict."

- r/ecommerce, u/AmazonSellerKing (390 upvotes, Feb 2026)

War Risk Insurance

Marine insurance premiums have surged over 300%. Before the crisis, insuring a vessel for Hormuz transit cost about 0.25% of hull value. It now exceeds 5%, a 20x increase from pre-Red Sea baselines. A $150 million LNG carrier pays roughly $1.5 million per voyage in war risk premiums alone. Several insurers have stopped underwriting the region entirely.

For e-commerce sellers, this means higher freight quotes across the board, even on routes that do not touch the Gulf. Insurance repricing is global.

Air Freight Is Not a Clean Escape

Sellers who try to air-freight around the disruption face their own cost wall:

- Shanghai to Frankfurt: EUR 6.50-8.50/kg, up from EUR 4.20-5.50 in Q4 2025 (35-60% increase)

- South Asia to Europe: up 70%

- Gulf airspace closures are pushing cargo onto longer detours through Central Asia and Turkey

- FedEx and UPS implemented fuel surcharges reaching 34% for international air exports

"Hormuz is the new Red Sea nightmare. With Iran threats escalating, 20% of ships rerouting via Africa, adding 10-14 days to Asia-Europe lanes. Ecom sellers, kiss your margins goodbye."

- r/supplychain, u/ShipChainPro (450 upvotes, Jan 2026)

Delivery Times: What Customers Will Actually Experience

The rerouting math is straightforward. Ships that cannot pass through Hormuz must go around the Cape of Good Hope, adding 3,500-4,000 nautical miles, 10-14 days of transit time, and 25-30% more fuel consumption per voyage.

Major platforms are already adjusting promises:

- Amazon: Delivery windows extended from 25-35 days to 35-45 days on affected routes

- Temu: Extended from ~15 days to ~20 days to Middle East destinations

- SHEIN: Extended from 5-8 days to 8-10 days

The worse impact comes in 2-5 weeks as diverted containers arrive in clusters, creating port congestion, drayage bottlenecks, and inventory gaps in warehouses that were expecting containers on the original schedule.

Which Products Get Hit Hardest

The Hormuz closure is fundamentally an energy crisis, and energy touches everything. But some product categories face disproportionate pressure.

"Real talk: ME conflict closed Hormuz lanes for my Vietnamese supplier. Switched to air, costs tripled ($15k vs $4k sea), 7-day delivery but margins gone. Sold out holiday inventory."

- r/FulfillmentByAmazon, u/FBAWarrior (550 upvotes, Dec 2025)

Plastics and Packaging

85% of polyethylene exports from the Middle East go through Hormuz. Polymer prices have surged 41-42% since February 28. PE producers are seeking price increases of $0.15-$0.20/lb through April. Since 40% of global plastic packaging goes to food and beverage, this affects nearly every physical product that ships in a box, bag, or blister pack.

Electronics

Shortages of helium and specialized gases from the Gulf are creating what industry analysts call a "near-immediate crisis" for semiconductor and advanced electronics production. AWS data centers in the UAE and Bahrain sustained damage, affecting Amazon Seller Central, advertising consoles, and order management systems.

Pharmaceuticals and Health Products

Chemical inputs for Indian generic drug manufacturing are consolidated through Dubai/UAE hubs. Shortages in diabetes drugs, hypertension treatments, and antibiotics are expected within 4-6 weeks. Nearly 50% of US generic prescriptions originate in Indian factories dependent on Gulf chemical inputs.

Fertilizers and Food

Roughly one-third of global fertilizer trade transits Hormuz. Urea prices jumped from $475 to $680 per metric ton, a 43% increase. Food price inflation is expected within 60 days of the disruption. Every e-commerce brand in the food and beverage category should be recalculating costs now.

The Margin Math: What a $10 Product Actually Costs Now

Here is the math that matters for e-commerce operators. Take a product with a $10 retail price:

- Pre-crisis landed cost: approximately $5.50 (product + shipping + duties)

- Post-crisis landed cost: shipping increases of $1.50-$2.00, packaging cost increases, fuel surcharges, insurance pass-through

- New landed cost: approximately $7.50-$8.00

On a product that sells for $10, your gross margin just dropped from roughly 45% to 20-25%. If you are running paid acquisition, that margin may not cover your customer acquisition cost.

Across the industry, 49% of brands report significantly increased landed costs, and 71% are raising prices. The question is not whether to adjust pricing, it is how fast.

Inflation Is Already Moving

Truflation's real-time CPI tracker shows consumer inflation jumping from 0.68% year-over-year on February 8 to 1.52% year-over-year by March 18. Prolonged closure could add 0.5-1.0 percentage points to full-year inflation forecasts. Goldman Sachs warned that if the closure persists, "inflation will become a permanent problem."

Countries and Markets Most Exposed

If you sell into or source from these markets, the disruption is direct:

- UAE: Jebel Ali port (9th largest globally) sustained missile damage. Amazon's Abu Dhabi fulfillment center is closed. Re-exports worth $163 billion disrupted.

- India: Imports 53% of LNG from Qatar/UAE. Maersk suspended all India-Upper Gulf bookings. Chemical inputs for pharmaceutical manufacturing cut off.

- Saudi Arabia: Dammam and Jubail container ports fully blocked on the Gulf coast.

- China: 40% of oil imports transit Hormuz. Asian petrochemical plants rely on Middle East for 70-80% of naphtha feedstock.

- Japan and South Korea: Major crude oil destinations. Nikkei 225 fell 11%. South Korean container freight rates jumped 30%.

- Pakistan and Bangladesh: 99% and 72% LNG import dependency respectively. Pakistan has moved to a 4-day government workweek to conserve fuel.

How This Compares to Previous Disruptions

| Factor | Suez 2021 | Red Sea / Houthi 2023-24 | Hormuz 2026 |

|---|---|---|---|

| Cause | Accident (ship grounding) | Houthi attacks | Military conflict / blockade |

| Duration | 6 days | Months (ongoing) | 3+ weeks (ongoing) |

| Maritime bypass? | Yes (Cape of Good Hope) | Yes (Cape of Good Hope) | No bypass exists |

| Oil price impact | Minimal | Moderate | $72 to $126/barrel |

| Global oil supply removed | Negligible | Negligible | 20% |

| Container shipping impact | Temporary delays | 90% decrease in Red Sea traffic | 95%+ collapse in Hormuz transit |

The critical difference: Houthi Yemen announced on February 28 that it would resume Red Sea attacks, creating a dual chokepoint crisis. Both the Suez/Red Sea corridor and the Hormuz corridor are simultaneously disrupted. This has never happened before.

What Happens Next: Analyst Projections

The timeline depends on whether and when a ceasefire holds. Capital Economics and Goldman Sachs model three scenarios:

- Short war (weeks): Oil settles to $65/barrel by year-end. Shipping normalizes in 2-3 months. Temporary price increases absorbed.

- Prolonged conflict (months): Oil averages $130/barrel in Q2, potentially $150 over six months. US GDP drops to 2.25%. Eurozone contracts. Inflation peaks above 4% in Europe, 3% in the US.

- Worst case (escalation): Oil approaches $200/barrel. Global recession. E-commerce discretionary spending drops significantly, mirroring the 2022 pattern where growth fell from 25.7% to 6.5%.

Iran is developing a "selective" vetting system for Hormuz transit: not a full reopening. Five European nations plus Japan have signaled readiness to contribute to securing the strait, contingent on a ceasefire. But negotiations are complicated by nuclear program demands, reparations, and sanctions relief.

What E-Commerce Sellers Should Do Right Now

This is not a wait-and-see situation. Costs are already higher. Inventory is already delayed. Here are the concrete steps that matter:

1. Reforecast Landed Costs This Week

Every SKU that depends on ocean freight needs a new landed cost calculation using current surcharges and fuel prices. Run two scenarios: oil at $100/barrel and oil at $130/barrel. Price accordingly.

2. Audit Every In-Transit Shipment

Know which vessels are carrying your inventory, what route they are taking, and whether they are affected by rerouting. If your freight forwarder cannot provide vessel-level tracking, you are operating blind.

3. Build Buffer Stock on Top Sellers

Safety stock calculations based on pre-crisis lead times are now wrong. Add 4-6 weeks of additional buffer stock on your highest-velocity SKUs. The cost of carrying extra inventory is less than the cost of stockouts during a supply chain crisis.

4. Update Delivery Promises on Your Storefront

Customers will tolerate longer delivery times if you set expectations upfront. They will not tolerate being promised 5 days and receiving their order in 15. Update estimated delivery dates now.

5. Diversify Away from Single-Source Supply Chains

If all your products come through one port, one carrier, or one region, you are exposed. Start conversations with suppliers in regions that do not depend on Hormuz. Our supply chain crisis playbook covers regional diversification strategies in detail.

6. Lock in Fuel and Freight Contracts Where Possible

Spot rates will get worse before they get better. If your 3PL or freight forwarder offers fixed-rate contracts, this is the time to negotiate, even at today's elevated prices.

7. Centralize Inventory Visibility Across Channels

When supply is constrained, you cannot afford to have inventory sitting unsold on one channel while another channel is out of stock. Real-time inventory sync across every sales channel becomes operationally critical during supply shocks. Centralized inventory solutions eliminate the blind spots that lead to overselling when shipments are delayed and stock levels are reduced.

The Bottom Line

The Strait of Hormuz crisis is the largest supply chain disruption since the 1970s energy crisis. It is not a temporary blip. Even optimistic scenarios project months of elevated costs and disrupted logistics.

E-commerce businesses that act now, recalculating costs, building buffer inventory, diversifying supply chains, and maintaining accurate inventory across channels, will absorb the shock. Those that wait for the crisis to resolve on its own will find their margins gone and their customers shopping elsewhere.

The data is clear. The question is whether you move on it.

Frequently Asked Questions

Container shipping surcharges have increased $1,500-$4,000 per container depending on the carrier. Hapag-Lloyd imposed a $1,500/TEU war risk surcharge, CMA CGM charges $2,000-$4,000 per container, and Maersk added emergency freight increases of $1,800-$3,800. War risk insurance premiums surged over 300%. These costs flow directly into landed costs for imported goods.

As of March 2026, Iran has begun selectively allowing some ships through under a vetting system, but transit volume remains at single digits per day compared to 138 vessels per day pre-crisis. Analysts project severe disruption for up to 6 months with only partial mitigation. Ceasefire negotiations are ongoing but complicated by nuclear, reparations, and sanctions demands.

Petrochemical-dependent products are hit hardest: plastics and packaging (polymer prices up 41-42%), synthetic clothing, cosmetics, and electronics casings. Fertilizer prices rose 43%, affecting food costs. Electronics face helium and specialty gas shortages from the Gulf. Any product with plastic packaging sees cost increases since 40% of global plastic packaging goes to food and beverage.

The Suez blockage in 2021 was a 6-day accident with an available bypass (Cape of Good Hope). The Hormuz crisis is a deliberate military blockade with no maritime bypass, lasting 3+ weeks and counting. It removed 20% of global oil supply versus minimal oil impact from Suez. Brent crude went from $72 to $126/barrel. The Hormuz crisis is fundamentally an energy crisis that compounds into a shipping crisis.

Build 4-6 weeks of additional buffer stock on top sellers. Reforecast landed costs weekly using dual fuel-price scenarios. Audit all in-transit shipments and confirm vessel routing. Diversify suppliers away from Hormuz-dependent regions. Shift toward regional sourcing where possible, and implement dynamic delivery date estimates on product pages to manage customer expectations.

Related Articles

View all

Shopify Just Democratized Wholesale. DTC-Only Brands Should Be Nervous

Shopify is bringing native B2B features to more merchants. That lowers the barrier to wholesale and pressures DTC-only brands to rethink channel strategy.

The DTC-Only Brand Is Dead. B2B Is the Comeback Channel

DTC brands are rediscovering B2B because paid acquisition is volatile and wholesale can create repeatable, larger, more predictable order flow.

AI Checkout Failed the First Test. Here's Why Shoppers Still Prefer Real Stores

AI shopping is moving fast, but checkout is proving harder than discovery. Retailers want AI traffic without surrendering the customer relationship.